Arconic (ARNC) - From Russia with Love

Arconic (ARNC) - From Russia with Love

Not your average metal bender

TLDR Twitter thread below:

Intro

The current market environment is not for the faint of heart. Fundamentals matter again and dispersion is the name of the game.

Outperforming longs have been narrowly confined to the energy complex (refiners, natural gas producers, oil names) and other commodities. Throw in some special sits for good measure.

The long playbook going forward is simple. We want to be long:

Free cash flow generators with pricing power at cheap absolute valuations.

Recession-resistant or recovering end markets.

Rock-solid balance sheets run by strong capital allocators buying back shares.

We want to be short almost everything else.

Arconic (ARNC) presents an under-the-radar opportunity to buy all of the above, with:

Organic investments driving double-digit EBITDA growth in recovering or recession-resistant end markets.

An inflection of free cash flow as the burden of legacy liabilities and working capital drag of soaring aluminum prices reverses, accelerating share repurchases and the initiation of a dividend in 2H22.

A cheap absolute and relative valuation at a ~15% normalized FCF yield and 1-2 turns below peers.

A call option on the resolution of their Russian asset.

I see shares at ~$44 by the end of 2023, representing > 60% upside.

Summary

Arconic (ARNC) is a downstream aluminum processor that passes through or hedges > 90% of the underlying commodity price. As a value-added converter, end market volumes, not commodity prices, are the driver of performance.

ARNC is highly levered to recovering and/or stable, growing end markets, with automotive, packaging, and aerospace representing ~60% of revenues. Despite the knock-on effects of the Russia/Ukraine war, continued semiconductor constraints, and a ~$40M FY22 EBITDA impact due to its Russian operations, ARNC raised its guidance in Q1 to reflect +15-22% Y/Y EBITDA growth in FY22.

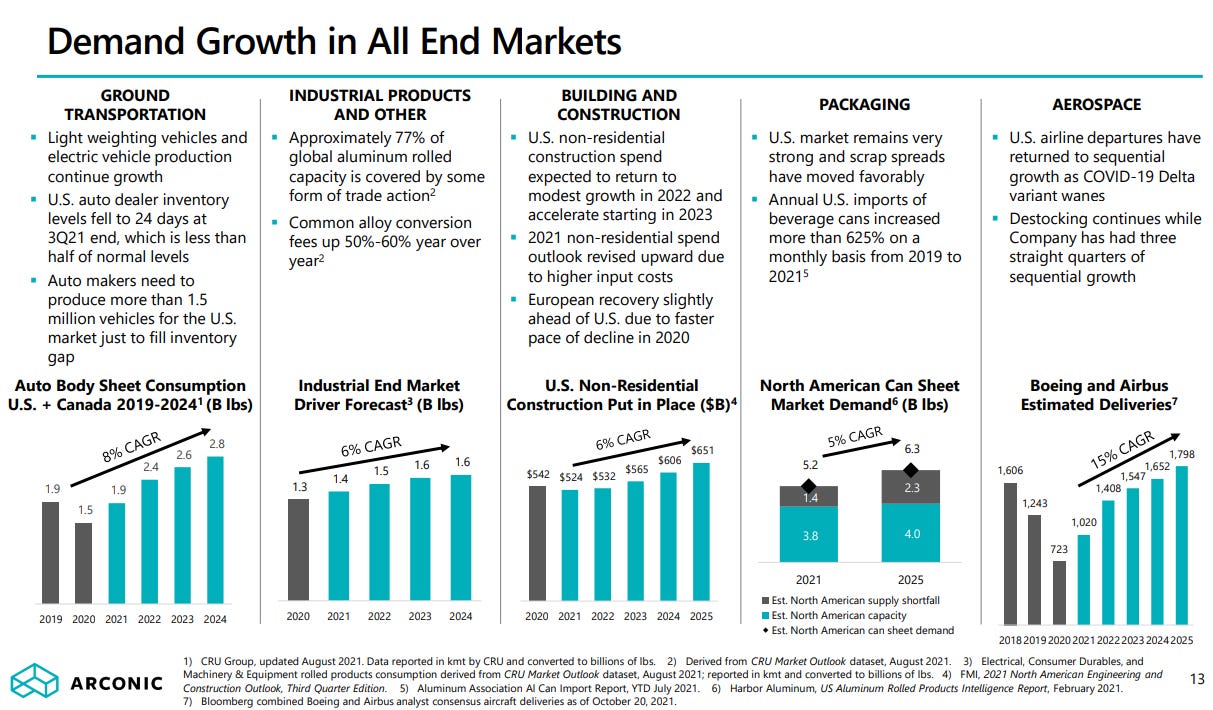

Automotive is by far its largest end market (33% of revenues) and continues to be impacted by semiconductor availability at its key customers. As the supply chain eases in the back half of the year and into 2023, ARNC will be a prime beneficiary of increased automotive production, leading to strong double-digit automotive growth over the next two years.

Secular trends including industry-wide increased aluminum adoption and increasing content per vehicle have driven new program wins, allowing ARNC automotive volumes to outperform NA Light Vehicle Production by 18% in 2021.

Aerospace revenues will grow ~30-40% this year and still be ~30% below pre-pandemic revenues. Aerospace is by far its highest margin end-market with 2-3x margins of the consolidated company, and a full aero recovery by 2024 would generate ~$100-$200M of incremental EBITDA vs. 2022.

The company recently re-entered the North American packaging market following the expiration of a non-compete with Alcoa. They have negotiated agreements with six can manufacturers representing $1.5B in expected revenue from 2022-2024, representing a 31% CAGR.

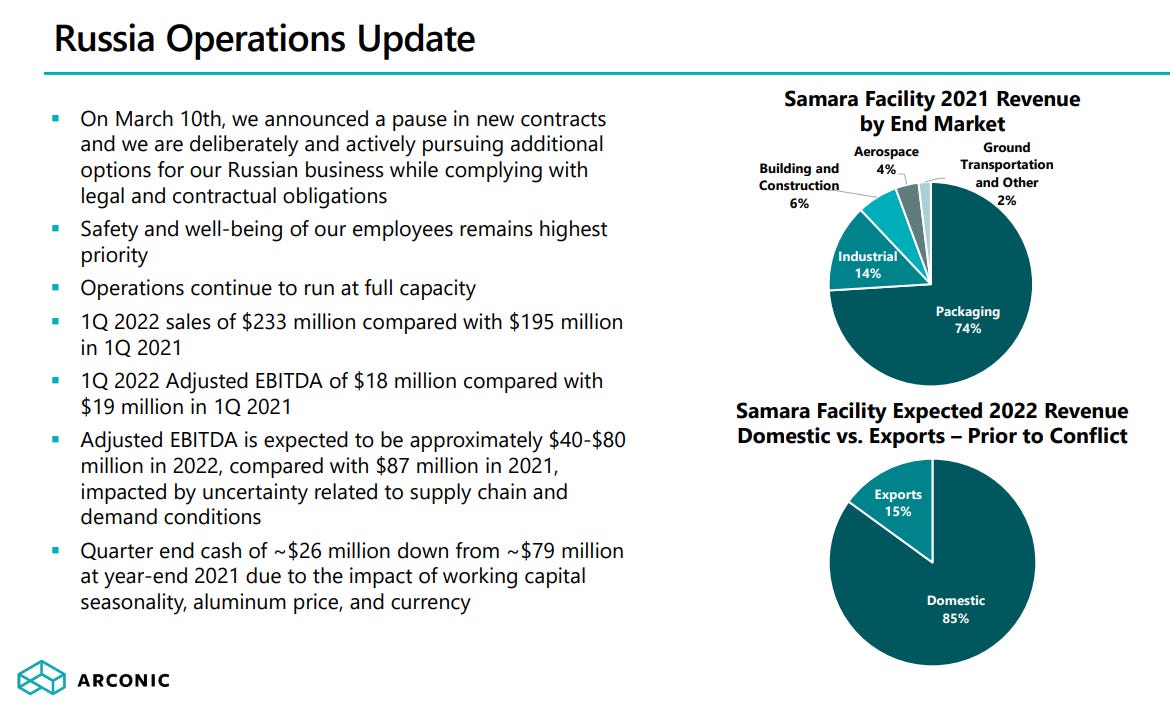

The Russian Samara facility, which generated $87M of EBITDA in 2021, is already marked to zero in sell-side and buy-side models. Any incremental proceeds from a sale represent a sizeable call option. Regardless of the outcome, the resolution will clear a key overhang on the shares.

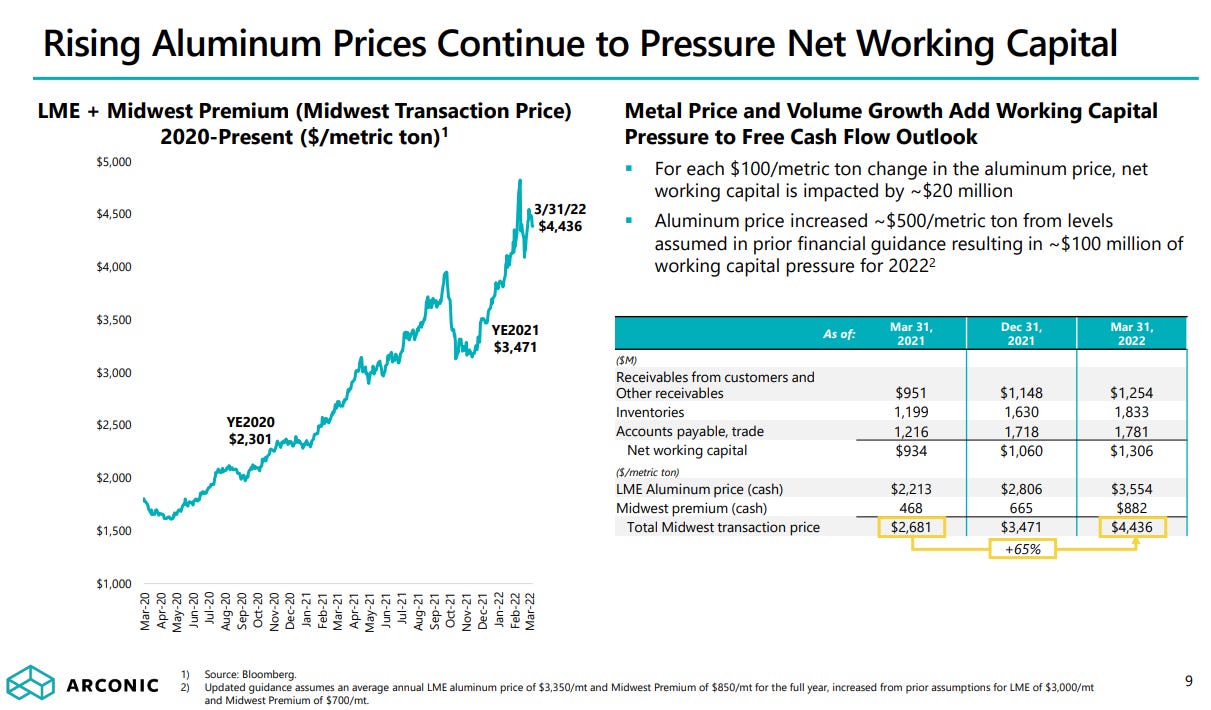

ARNC’s working capital was hit hard by the parabolic increase in aluminum prices. That headwind will turn into a > $300M+ tailwind to FCF going forward, and combined with the reduction in growth capex and legacy liabilities, will allow the company to accelerate share repurchases and initiate a dividend in 2H22.

The balance sheet has been de-risked since separation, with net after-tax pension and OPEB liability down to $900M from $1.5B. Combined pension contributions, OPEB, and environmental payments have been reduced from $408M in 2020 and $581M in 2021 to ~$80M going forward.

Downstream aluminum processors tend to have fairly stable valuations, with EBITDA multiples in the 6-8x range. Given its limited trading history, Grenfell liability risk, and Russian Samara exposure, ARNC is currently trading at ~5.5x 2022 EBITDA vs. close peer Constellium (CSTM) at ~6.5x. Assuming zero multiple appreciation, I see ARNC shares at ~$44 by the end of 2023, representing > 60% upside. A multiple re-rate to CSTM’s would be icing on the cake.

Overview and History

Arconic (ARNC) is a specialty aluminum converter. They buy primary or scrap aluminum at the LME price, covert it into a finished product, and then sell that finished product to customers. This is a value-added conversion business with 90%+ of aluminum price exposure passed along or hedged, and the final pricing of the product reflects changes in the price of aluminum including regional premiums.

Arconic was originally spun out of Alcoa in 2016 and included the engineered products business comprised of the Engines, Fastening Systems, Engineered Structures, and Forged Wheels businesses. In 2019, the engineered products business was split from Arconic and re-named Howmet Aerospace (HWM). To the delight of HWM investors, CEO John Plant stayed on as CEO of HWM.

The current ARNC business is comprised of three segments: Rolled Products (83% of FY21 sales), Building and Construction Systems (13% of FY21 sales), and Extrusions (4% of FY21 sales). Assuming zero contribution from its Russian Samara asset, 71% of ARNC’s revenues come from the US, 10% from China, 16% from Europe, and 3% from other countries.

ARNC has a unique and irreplaceable asset base, including the world's largest thick plate stretcher and the world's largest aluminum-lithium plant. They are the only supplier in the world able to produce single-piece aluminum-lithium wing skins. Their Davenport facility, which has an estimated replacement cost of $8-$10B, has supplied 100% of Boeing wing skins for decades.

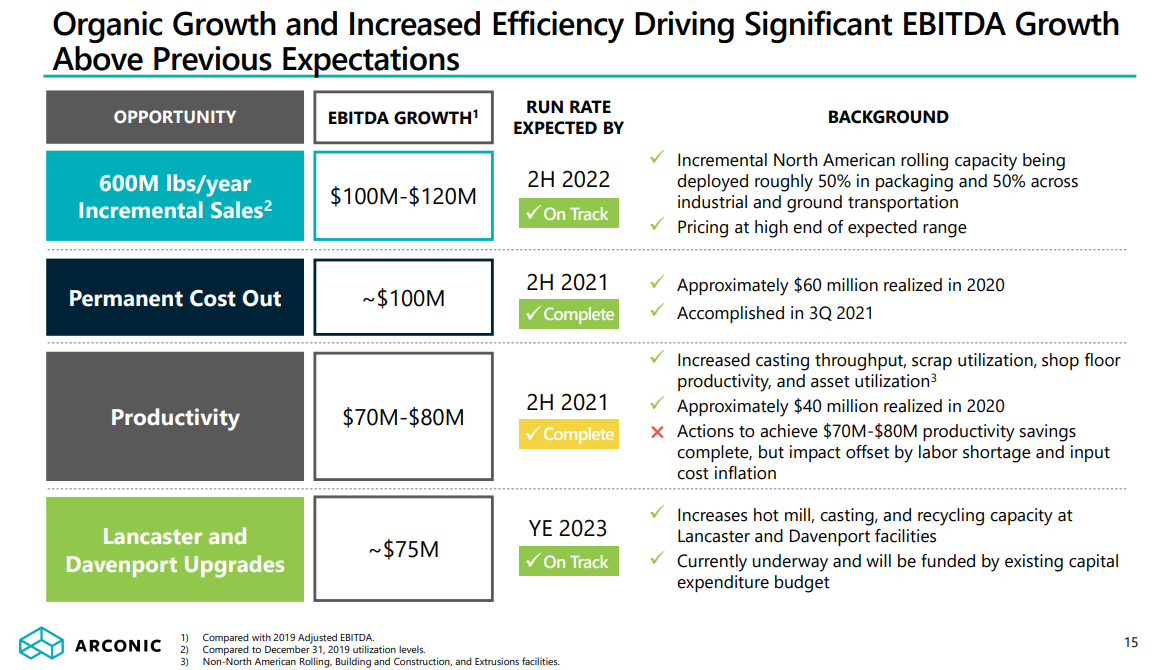

Over the past eight years, the company has been focused on shifting its mix to newer markets with secular tailwinds and higher margins. Continued light weighting in aerospace, rising use of aluminum in vehicles, advancement of code in building and construction, the ongoing shift to aluminum cans over plastic and glass in packaging, as well as ~$1.1B in major capital investments have driven a step function change in expected revenue growth and realized EBITDA/ton.

ARNC is well positioned to grow Adj. EBITDA double-digits annually for the next few years driven by strong end-market growth and mix, even in a recessionary scenario:

Prime Beneficiary of Increased Automotive Production

Ground Transportation (Automotive) is ARNC’s largest end market (33% of revenues) and supplies aluminum products to OEM’s and Tier 1 suppliers around the world, with Ford as its biggest customer. Like other auto suppliers, the business continues to be impacted by semiconductor availability at its key customers. As supply chain constraints ease in the back half of the year and into 2023, ARNC will be a prime beneficiary of increased automotive production, leading to > double-digit growth over the next two years.

The longer-term story for ARNC automotive is bright. Secular trends including industry-wide increased aluminum adoption and increasing content per vehicle have driven new program wins, allowing ARNC automotive volumes to outperform NA Light Vehicle Production by 18% in 2021. Behind aerospace, automotive is also the second-highest margin segment in ARNC’s portfolio. If you’ve been looking for a way to play the auto production rebound but think supplier margins are at risk, ARNC is a safe bet.

Highest Margin Aerospace Recovery

Aerospace revenues grew +32% Y/Y in Q1 and management’s outlook for Q2 is even better. Revenues will grow ~30-40% this year and still be ~30% below pre-pandemic revenues. Importantly, management believes they reached the end of destocking in Q1 and continue to expect aerospace revenues to reach pre-pandemic levels sometime in 2024. Aerospace is by far its highest margin end-market with 2-3x margins of the consolidated company, and a full aero recovery by 2024 would generate ~$100-$200M of incremental EBITDA vs. 2022.

Another Way to Play the Aluminum Can Thesis

Following the expiration of a non-compete with Alcoa in October 2020, ARNC has re-entered the North American packaging market. ARNC expects half of the 600M lbs of additional capacity at its Tennessee facility to be allocated to packaging. US can sheet demand is expected to grow at a 5% CAGR through 2025, and additional can lines announced by can manufacturers represent incremental can sheet demand of ~1.2B pounds over the next four years. ARNC has negotiated agreements with six can manufacturers representing $1.5B in expected revenue from 2022-2024, representing a 31% CAGR. Packaging revenue represents locked-in, recession-resistant, and secularly growing revenues.

Organic Investment Opportunities Driving EBITDA Growth

ARNC has invested ~$1.1B in major capital investments since 2013 and these initiatives are now nearing completion, with EBITDA growth expected to benefit in 2023 and beyond. Alongside the mix shift to higher-margin and growing end markets, a variety of internal projects are nearing an end and will drive > $350M run-rate EBITDA benefit by the end of 2023.

I estimate ARNC run-rate EBITDA in 2024 will be ~$950M. For perspective, the sell-side has them at > $1B in 2024 with Samara zeroed out. I believe these will prove to be overly conservative, and we will get an updated long-term EBITDA target at their upcoming Investor Day on June 6th.

FCF Inflection and Capital Allocation Optionality

ARNC’s working capital has been hit hard by the recent parabolic increase in aluminum prices. That headwind will turn into a > $300M+ tailwind to FCF going forward, and combined with the reduction in growth capex and legacy liabilities, will allow the company to accelerate share repurchases and initiate a dividend in 2H22.

Since the quarter ended 3/31/22 until their Q1 earnings call on 5/4/22, the Midwest Transaction Price per metric ton has decreased from $4,436 to ~$3,800, freeing up > $120M of FCF. Despite a ~$185M working capital drag, the company is guiding for ~$125M of levered FCF for the year. Given the recent drop in aluminum prices, they should be revising their FCF guidance upwards during their investor day or next quarter.

The balance sheet has also been de-risked since separation, with net after-tax pension and OPEB liability down to $900M from $1.5B. Combined pension contributions, OPEB, and environmental payments have been reduced from $408M in 2020 and $581M in 2021 to ~$80M going forward.

On a normalized basis assuming no working capital drag and maintenance capex of ~$145M, levered FCF is in the ~$450M range against a market cap of ~$3B, implying a ~15% normalized FCF yield.

Comps and Valuation

Downstream aluminum processors tend to have fairly stable valuations, with EBITDA multiples in the 6-8x range. Constellium (CSTM), Kaiser (KALU), and ARNC are very similar in terms of margins and EBITDA/ton. Historically, Kaiser enjoyed a higher multiple as a result of higher margins due to its material aero exposure, but the addition of packaging to its portfolio through its Warrick acquisition should increasingly converge multiples across the board.

Given its limited trading history, Grenfell liability risk, and Russian Samara exposure, ARNC is currently trading at ~5.5x 2022 EBITDA vs. close peer CSTM at ~6.5x and KASU at ~7.5x. I believe this discount is unwarranted given ARNC’s idiosyncratic drivers and balance sheet transformation. ARNC should trade at 6-7x EBITDA or a 10-15% normalized FCF yield once the Russian/Grenfell overhangs are cleared. However, assuming zero multiple appreciation, I see ARNC shares at ~$44 by the end of 2023 using a 5.5x EBITDA multiple on 2024E EBITDA of ~$950M, representing > 60% upside. This only assumes $315M of incremental share repurchases through 2023 - I believe there’s > $150M (> $2/share) incremental upside there. There’s plenty of conservatism built in here for any economic scenario. and downside is relatively truncated given recovering end markets, FCF inflection, and capital allocation optionality. A multiple re-rate to CSTM’s would simply be icing on the cake.

Risks

Russian Samara Asset

Unfortunately for ARNC, they have Russian exposure through their Samara asset, which generated $87M of EBITDA in 2021. On 5/19/22, ARNC announced that they’re pursuing a sale of its Russian operations following a review of strategic alternatives, and that they expect to record a charge of up to $500M. Despite the ongoing war, Samara still generated $18M of EBITDA in 1Q22 and was expected to generate $40-$80M in 2022. Following the start of the conflict, I believe most of the buy-side and sell-side marked it as a zero. I’m doing the same but any proceeds represent a decent size call option on the stock.

Grenfell Liability Risk

In June 2017, a housing block in London caught fire, killing 72 people. At the time, ARNC’s ParentCo supplied Reynobond PE, a cladding product, to a fabricator, which supplied an installer. The first phase of the inquiry by the UK government found that the cladding acted like a “source of fuel” for the fire, which ripped up the sides of the tower, leading to the deaths of 72 people.

The second phase of the inquiry is on-going:

As Phase 2 of the public inquiry continues, the testimony has supported AAP SAS’s position that the choice of materials and the responsibility of ensuring compliance of the cladding system with relevant U.K. building code and regulations was with those individuals or entities who designed and installed the cladding system such as the architects, fabricators, contractors and building owners. The ongoing hearings in the U.K. have revealed serious doubts about whether these third parties had the necessary qualifications or expertise to carry out the refurbishment work at Grenfell Tower, adequately oversaw the process, conducted the required fire safety testing or analysis, or otherwise complied with their obligations under U.K. regulations. AAP SAS is participating as a Core Participant in the Public Inquiry and is also cooperating with the ongoing parallel investigation by the Police. Arconic Corporation does not sell and ParentCo previously stopped selling the PE product for architectural use on buildings.

We don’t have much to go off of here, but management feels that they’re adequately insured from previous ParentCo. My view - this is not a liability with uncapped downside like PFAS for DuPont/3M, and it’s one of the main reasons ARNC has a multiple turn below peers. A turn on the EBITDA multiple is worth close to ~$1B, so I think it’s appropriately baked in with some room for relief.

Catalysts

Upcoming Investor Day on June 6th (raise FCF guidance and detail long-term targets)

Accelerated share repurchases

Initiation of dividend in 2H22

Sale proceeds from Samara

Resolution of Grenfell

Thanks for the writeup. This is very interesting. One question: how stable is the demand for aluminum processing? It seems to me that aluminum processing can be linked to consumption cycle.