Weekend Links

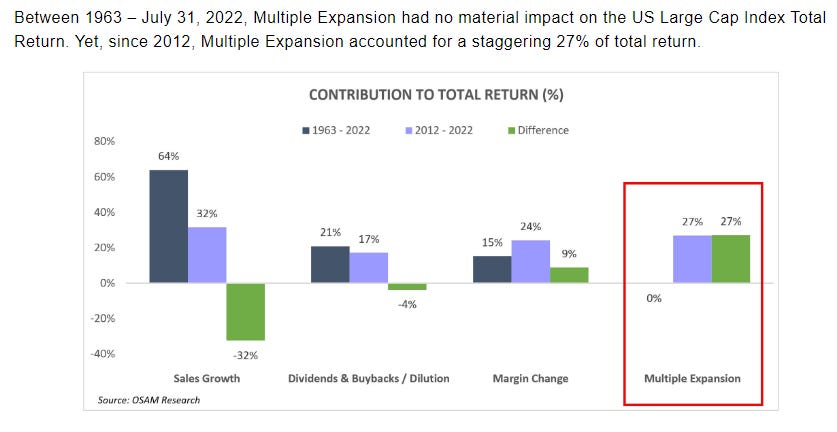

The Increasing Importance of Multiple Expansion

Chart of the Week - The Increasing Importance of Multiple Expansion

via Jamie Catherwood, O’Shaughnessy Asset Management (article below)

Why Fundamentals Matter

via Jamie Catherwood, O’Shaughnessy Asset Management

Since Multiple Expansion has become a key driver of total returns, a significant portion of the equity market’s return is now derived from a “speculative” component based on expectations. As discussed, this speculative component is influenced by the powerful narratives used to entice investors.

For example, at the beginning of the pandemic, when many people were preaching that life as we knew it had irrevocably changed (e.g., no more in-person meetings, the death of business travel, etc.), shares of work-from-home stocks like Zoom traded at 464.8x next year’s earnings.

However, investors should remember that companies primarily generating returns from multiple expansion are susceptible to wild swings because this is the least tangible source of total return. A company’s earnings don’t change on a whim, but investors’ willingness to pay higher multiples for the same stock do.

This is a great irony of the speculative feedback loop described earlier. When asset prices are rising, investors typically require less conviction or belief in an asset to purchase it. When prices are falling, however, investors meticulously study the merits of an investment and make sure they have strong conviction in its prospects.

When that happens, it’s often too late to try and increase earnings or bolster other important fundamentals that were left ignored for far too long.

Unsound play & the value of speed

via Variance Swap’s Substack (Variances)

Balancing when you can “play unsoundly” and when you must thoroughly know an asset in question (and its value) will forever be a challenge to the generalist. It is very easy to overestimate your own knowledge of an asset and overvalue your own background knowledge when, more often than not, the market knows far more than you.

When handling other peoples’ money, defaulting to a thorough and detailed approach to public markets investment should be the norm. It is my personal default approach. I have tried my hand at playing unsoundly to mixed results. I prefer to understand the ins-and-outs of an asset I’m purchasing, underwrite a downside scenario that’s reasonable, and evaluate the probability of it occurring conservatively.

What Does It Mean To Be A Good Stock Picker? Part 2

by Cameron Height of Alpha Theory

Slugging percentage is a measurement of the average winner divided by the average loser. If I have a batting average of 50% and a slugging of 1.0x, then my fund will generate a 0.0% return (50% of stocks make +20% and 50% make -20%). Anything greater for either of those metrics and the returns turn positive. If you can find winners that go up twice as much as losers, you need only have a batting of 33.3% to result in a return of 0.0%.

To demonstrate skill, a manager needs a slugging percentage* of 1.65x. This may seem high, but we must understand that the market demonstrates persistent positive skew (a straightforward way to think of positive skew is that more stocks go up more than 100% than go down more than 100%). This positive skew is also one of the major reasons that the batting average of the randomized portfolio we calculated in the previous post, 37.8%, seems so low.

Is Value Just an Interest Rate Bet?

by Cliff Asness of AQR

While not a proof, I’d point to the near non-existence of a correlation between value versus growth and interest rates over the long term as at least evidence very consistent with my math showing the durations of the two portfolios are simply not that different. In other words, when the empirical results line up with the math and concept, it’s likely you are on to something (or, in this case, on to disproving something) and any short-term changes, especially if unmet by changes in the math or assumptions, are therefore likely chance.

Frankly, the assumption of so many pundits who state, when value versus growth has been trading correlated to interest rates and they desperately need something to say, that it makes perfect sense as growth cash flows are much longer dated, is just wrong. They should stop repeating this easy, facile, mistaken and misleading observation. I predict as much success in my effort to change the dialogue here as I normally achieve!

So, why has value versus growth been trading the way it has in recent times? Put simply, I don’t know. Correlation, like fertilizer, happens. But that won’t stop me from taking a guess. If we’re in a bubble, then many must be assuming their growth portfolio is more like the unicorn example above than what real life has ever delivered.

If they believe that, it then follows they also believe growth stocks are considerably longer duration than normal relative to value stocks (recall that the unicorn was the only way to get any decent duration difference, though even there it’s less dramatic than many assume). Thus, if we are in a bubble, the very same bubble driving price differentials could rationally (rationally in the sense of consistent logic only after very irrational assumptions about growth) be expected to cause value to trade more correlated to interest rates than usual. Thus, a duration effect could arise from investors’ (temporarily exaggerated) belief in long-term growth differentials, even if only near-term growth differentials are likely to materialize. In other words, the very high (tech bubble level) prices being awarded to growth versus value stocks, and the realized correlation of value versus growth and interest rates, could easily be the same bubble showing up in different ways.25 That, or random chance – everyone’s least favorite explanation, but often the right one.

Maximum Drawdown as Predictor of Mutual Fund Performance and Flows

by Timothy Riley and Qing Yan

Mutual funds’ maximum drawdowns are persistent, indicative of manager skill, and predictive of subsequent performance. Among funds with relatively strong past performance, those with relatively low past maximum drawdowns, on average, have an out of sample alpha of 2.40% per year. That alpha is magnified when markets are turbulent—a time during which manager skill should be most valuable. Investors are averse to drawdown risk. After controlling for typical measures of past performance, fund flows remain a decreasing function of maximum drawdowns, particularly among investors with greater risk aversion and during times of heightened risk aversion.

The Logic of Envy - Sadly, Porn by Edward Teach, M.D. (AKA The Last Psychiatrist)—A Review

by Rob Henderson

The book states that “what shapes a person’s character isn’t his internal state, nor the sum total of his past experiences—though something like trauma may be relevant if it is used as something to overcome—character is formed by action only, and only in response to conflict. Literally nothing else matters.”

Men would rather believe themselves to be weak and pathetic than become the person their partners could depend on for satisfaction and love. “Why should she be satisfied by you?” Teach rhetorically asks. “After all—she hasn’t satisfied you.”

The book isn’t to make you happier. It’s to help make everyone else around you less miserable.

Asking what your actions mean is a defense. Ask instead: what do your actions get you out of? What do they allow you to do?

One of Teach’s most interesting challenges to the reader:

Describe yourself: your traits, qualities, both good and bad.

Do not use the word ‘am.’

Practice this.

His message in the book: “If you live your life with a ledger your bottom line will always sum to rage.”

So what can you do?

The Last Psychiatrist provides an answer in a post from 2009:

“No one ever asks me, ever, ‘I think I’m a narcissist, and I’m worried I’m hurting my family.’ If that was what they asked, I would tell them them change is within grasp. But…’I feel like I am playing a part, that I’m in a role. It doesn’t feel real.’ Instead of trying to stop playing a role – again, a move whose aim is your happiness – try playing a different role whose aim is someone else’s happiness. Why not play the part of the happy husband of three kids? Why not pretend to be devoted to your family to the exclusion of other things? Why not play the part of the man who isn’t tempted to sleep with the woman at the airport bar? ‘But that’s dishonest, I’d be lying to myself.’ Your kids will not know to ask: so?”

Skills Plateau Because Of Decay And Interference

by Scott Alexander (Astral Codex Ten)

Economist Philip Frances finds that creative artists, on average, do their best work in their late 30s. Isn’t this strange? However good a writer is at age 35, they should be even better at 55 with twenty more years of practice. Sure, middle age might bring some mild proto-cognitive-impairment, but surely nothing so dire that it cancels out twenty extra years!

A natural objection is that maybe they’ve maxed out their writing ability; further practice won’t help. But this can’t be true; most 35 year old writers aren’t Shakespeare or Dickens, so higher tiers of ability must be possible. But you can’t get there just by practicing more. If achievement is a function of talent and practice, at some point returns on practice decrease near zero.

The same is true for doctors. Young doctors (under 40) have slightly better cure rates than older doctors (eg 40-49). The linked study doesn’t go any younger (eg under 35, under 30…). However, Goodwin et al find that only first-year doctors suffer from inexperience; by a doctor’s second year, she’s doing about as well as she ever will. Why? Wouldn’t you expect someone who’s practiced medicine for twenty years to be better than someone who’s only done it for two?

We find the same phenomenon in formal education; on a standardized test of book learning for student doctors, there’s a big increase the first year of training, a smaller increase the second year, and by year 4-5 the increase is basically indistinguishable from zero (even though some doctors remain better than others). And here I talk about a slightly different phenomenon: ADHD children given Ritalin study harder and better, but haven’t learned any more vocabulary words at the end of a course (even though they haven’t learned all the vocabulary).

After a lot of looking through the psychological literature, I’ve found two hypotheses which, combined, mostly satisfy my curiosity.